Nationwide

Jarod Coulter, Valerie Grossman, Enrique Martínez-García, Peter C.B. Phillips and Shuping Shi

March 29, 2022

Precise house costs—costs adjusted for inflation—have progressively increased within the U.S. since 2012. Extra acceleration within the trot of house-trace appreciation started sooner than the pandemic nonetheless has bolstered noticeably since early 2020.

For possible traders and sellers to boot to policymakers, sparkling the narrate of housing markets is imperative. The use of a novel statistical toolkit for assessing the health of the U.S. housing market in valid time, we argue that the underlying causes of the flee-up fluctuate from those over the final housing boost, which preceded the 2007–09 World Monetary Crisis. On the synthetic hand, there might be rising roar that U.S. house costs are yet one more time changing into unhinged from fundamentals.

Table of Contents

Monitoring Emergence of Housing Bubbles in Precise Time

An asset—on this case, housing—is within the principle expansionary phase of a bubble when trace rises are out of step with market fundamentals. Rapid valid house-trace appreciation, such as that seen now, would not in itself imprint a bubble. Shifts in disposable income, the price of credit rating and safe entry to to it, supply disruptions, and rising labor and raw constructing gives charges are among the many financial causes for sustained valid house-trace beneficial properties.

Nonetheless valid house costs can diverge from market fundamentals when there might be well-liked perception that as of late’s tough trace will enhance will proceed. If many traders share this perception, purchases rising from a “be troubled of missing out” can drive up costs and heighten expectations of proper house-trace beneficial properties.

This self-pleasurable mechanism ends in trace narrate that might perchance perchance well also turn into exponential (or explosive), resulting within the housing market changing into gradually misaligned from fundamentals till investors turn into cautious, policymakers intervene, the waft of cash into housing dries up and a housing correction or even a bust occurs.

Expectations-pushed explosive appreciation (in general called exuberance) in valid house costs has many consequences, including the misallocation of enterprise property, distorted investment patterns, particular person bankruptcies and mammoth macroeconomic results on narrate and employment. Monitoring the housing market in valid time for the emergence of such booms in costs can back investors and policymakers acknowledge sooner than misalignments turn into so severe that subsequent corrections originate financial upheaval.

Time series of valid house costs that glean episodes of expectations-pushed bubbles present two necessary properties—they are nonlinear when graphed as a consequence of they are explosive true by their boost (or exuberant) phase, and they result in a correction and even a collapse if the market crashes.

To present market diagnostics, the Dallas Fed’s International Dwelling Label Database personnel, in partnership with a network of students from around the enviornment participating beneath the International Housing Observatory, produces datasets and statistics that suppose possible market exuberance. The methodology uses unique statistical suggestions to always computer screen housing markets—within the U.S. and around the enviornment—to detect symptoms and imprint the presence of rising housing booms.

Signs of a Market Tipping Level

When the statistics derived from these tactics are significant, the classes are date-stamped to signify exuberance—costs rising at an exponential price exceeding what financial fundamentals would clarify. The indicators are computed quarterly. A take a look at final result above a 95 p.c threshold signifies 95 p.c self perception of abnormal explosive habits, or housing market fever.

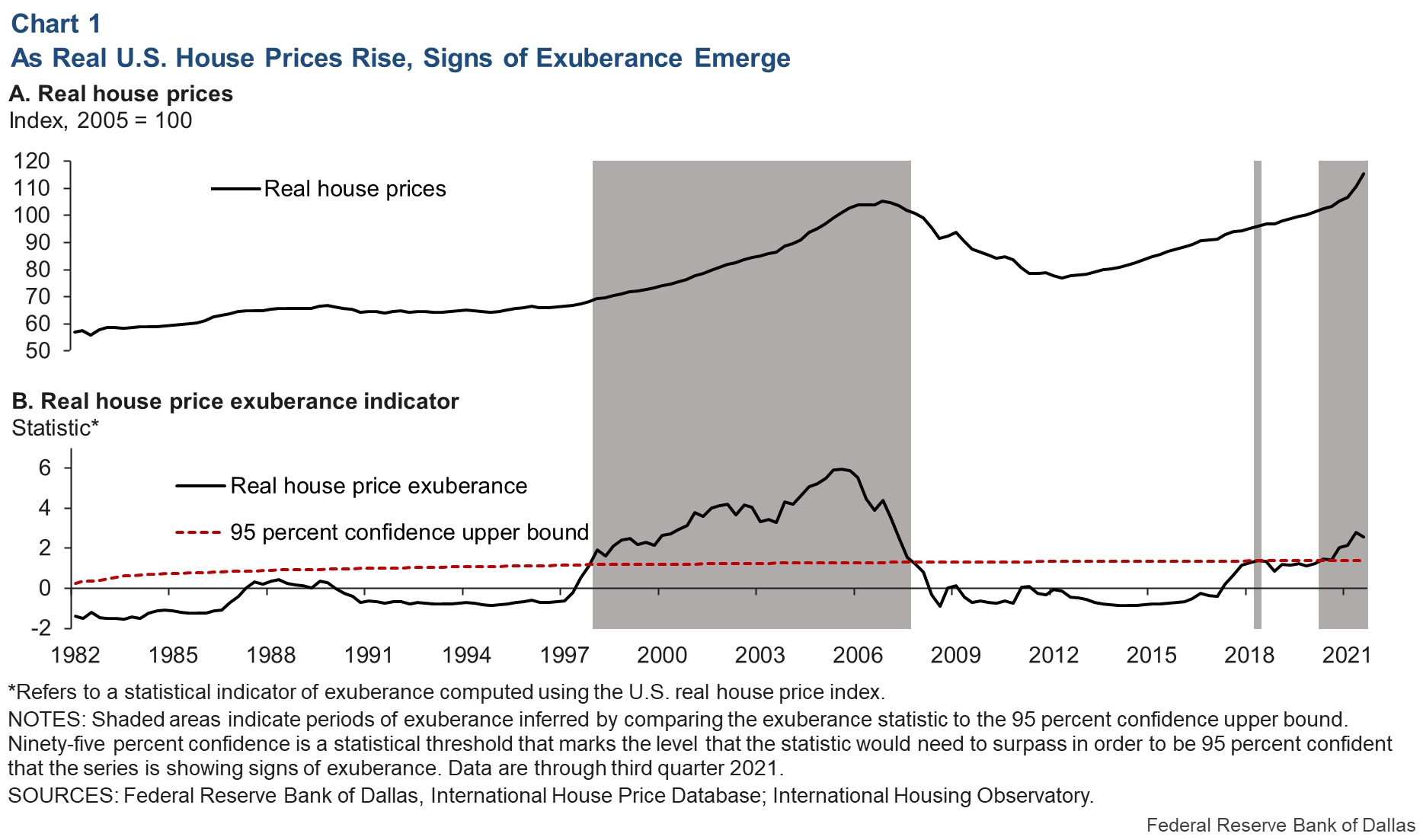

The history of the U.S. exuberance indicator is shown in opposition to the 95 p.c threshold in Chart 1. The statistic plotted within the bottom panel delivers a market temperature reading, esteem that from a non-public thermometer. The exuberance indicator presentations the temperature, and the self perception greater plod is the abnormality threshold. Basically the most unusual reading indicates that the U.S. housing market has been exhibiting indicators of exuberance for bigger than 5 consecutive quarters by third quarter 2021.

Downloadable chart | Chart info

The U.S. is no longer on my own in experiencing housing market fever. Eleven of the 25 international locations within the Dallas Fed’s International Dwelling Label Database present indicators of valid house-trace exuberance.

A Diagnostic Method to U.S. Housing Markets

To assess U.S. house costs true by the pandemic, we first fabricate an empirical relationship between house costs and those financial fundamentals underpinning the market, based on info by fourth quarter 2019. The theoretical benchmark is the conventional price of housing in accordance with the sum of discounted future rents. Right here’s same to the finance tenet that the conventional price of a firm’s inventory is the waft of future dividends discounted by the price of capital. (Analogously, the firm right here’s a rental, and its dividends are rents which might perchance perchance well be discounted by hobby rates.)

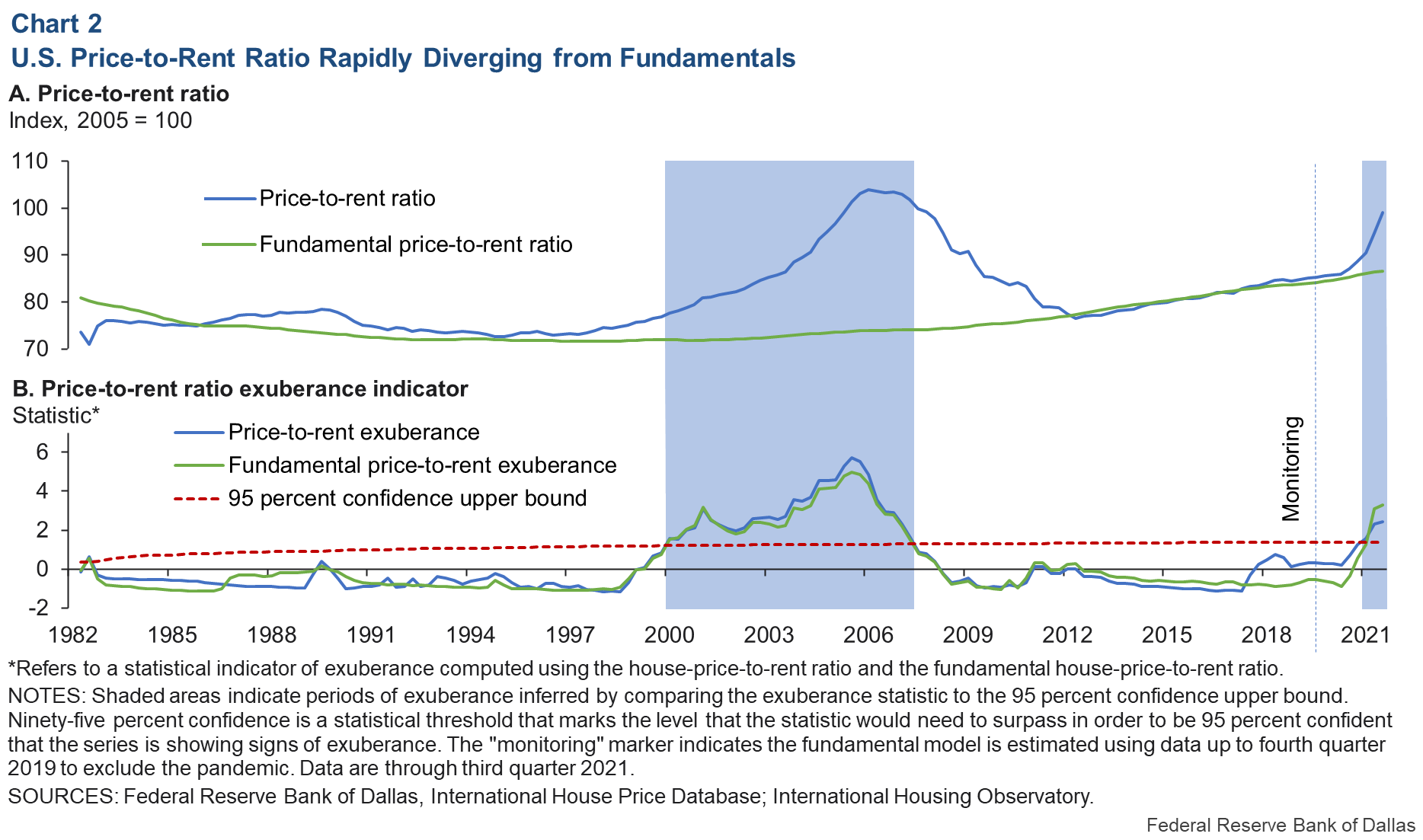

Working from that benchmark, the home-trace-to-rent ratio is printed by a miniature space of lagged financial variables, such as personal disposable income per capita, housing rents and long-term hobby rates. The residual of the regression, after placing off the outcomes of fundamentals, is classed for any remaining evidence of explosive habits. The upshot: Since the initiating place of 2020, the price-to-rent ratio has soared beyond what seen fundamentals on my own can level to (Chart 2).

Downloadable chart | Chart info

The gap between the valid trace-to-rent ratio and its traditional-based level within the U.S. has grown impulsively true by the pandemic—equivalent to the flee-up of the final housing boost—and started exhibiting indicators of exuberance in 2021. The exuberance statistic confirms that contemporary will enhance are some distance from current.

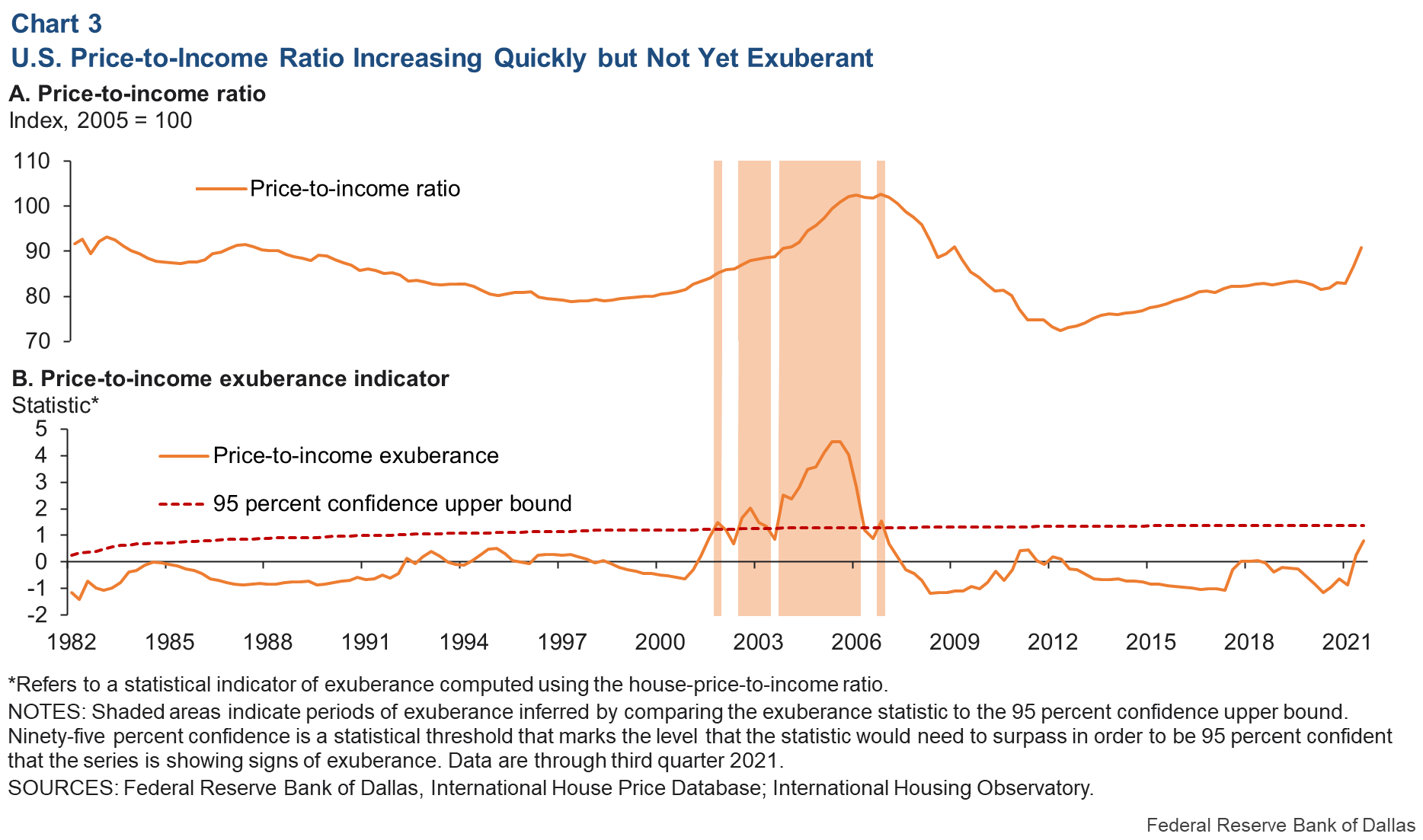

One other necessary long-flee anchor—tied in the present day to housing affordability—is the ratio of house costs to disposable income. Chart 3 presentations dates of episodes of exuberance for this measure of housing affordability. These info—not like our old metrics—operate no longer yet present evidence of explosiveness within the third quarter of 2021. Nonetheless the like a flash lengthen within the statistic discontinuance to the threshold true by 2021 indicates that U.S. valid house costs might perchance perchance well also quickly turn into untethered from personal disposable income per capita.

Downloadable chart | Chart info

The prolong in elevation of this exuberance statistic is partly the wreck result of a surge in valid disposable income true by the pandemic that ended in slower narrate rates within the price-to-income ratio. The surge in disposable income is largely associated to pandemic-associated fiscal and monetary stimulus efforts and reduced family consumption rising from mobility restrictions and lockdowns.

If disposable income will enhance flip out to be transitory—as fiscal stimulus wanes and the Federal Reserve reverses its accommodative monetary policy—contemporary patterns within the price-to-income ratio might perchance perchance well also tag a much less-precious measure of housing affordability. Such transitory will enhance in disposable income are no longer proper determinants of long-term housing investment. Thus, the price-to-income ratio measure on my own might perchance perchance well also originate overly conservative results when identifying housing market bubbles.

One other U.S. Housing Bubble Brewing?

Our evidence factors to abnormal U.S. housing market habits for the principle time since the boost of the early 2000s. Reasons for roar are sure in sure financial indicators—the price-to-rent ratio, in explicit, and the trace-to-income ratio—which present indicators that 2021 house costs seem more and more out of step with fundamentals.

Whereas traditionally low hobby rates are a component, they invent out no longer fully level to housing market developments. Assorted drivers have played a characteristic, including pandemic-associated U.S. fiscal stimulus programs and COVID-19-associated supply-chain disruptions and associated policy responses. The resulting traditional-pushed greater house costs might perchance perchance well even have fueled a be troubled-of-missing-out wave of exuberance inspiring new investors and more aggressive speculation among contemporary investors.

Based completely on most unusual evidence, there might be not one of these thing as a expectation that fallout from a housing correction would be equivalent to the 2007–09 World Monetary Crisis by methodology of magnitude or macroeconomic gravity. Among other issues, family balance sheets seem in better form, and frightful borrowing doesn’t seem like fueling the housing market boost.

Importantly, experience from the housing bubble within the early 2000s and the next pattern of evolved instruments for early detection and deployment of warning indicators—some illustrated on this diagnosis—mean that market participants, banks, policymakers and regulators are all better geared up to assess in valid time the significance of a housing boost. Thus, they are in a more-told location to react like a flash and keep away from essentially the most severe, negative consequences of a housing correction.

Referring to the Authors

Jarod Coulter

Coulter is a compare analyst within the Compare Department at the Federal Reserve Bank of Dallas.

Valerie Grossman

Grossman is a researcher and the accumulate scream material supervisor within the Compare Department at the Federal Reserve Bank of Dallas.

Martínez-García is a senior compare economist and advisor within the Compare Department at the Federal Reserve Bank of Dallas.

Peter C.B. Phillips

Phillips is Sterling Professor Emeritus at Yale University and a renowned professor at the University of Auckland.

Shuping Shi

Shi is a professor of economics at Macquarie University in Sydney, Australia.

The views expressed are those of the authors and might perchance perchance well also light no longer be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

{kind=link}

{kind=link}

{kind=link}